Healthcare regained its footing in Q2 2026, with valuations and equity returns improving across most of the industry after a year of uneven performance.

A powerful rebound in managed care anchored the quarter, while drug developers built on already strong momentum.

Capital returned to the space in force, and dealmaking accelerated to its highest pace in more than a year. Even the sectors still working through pressure showed early signs of stabilizing, leaving the industry in a healthier position as it enters the second half.

Sector Performance

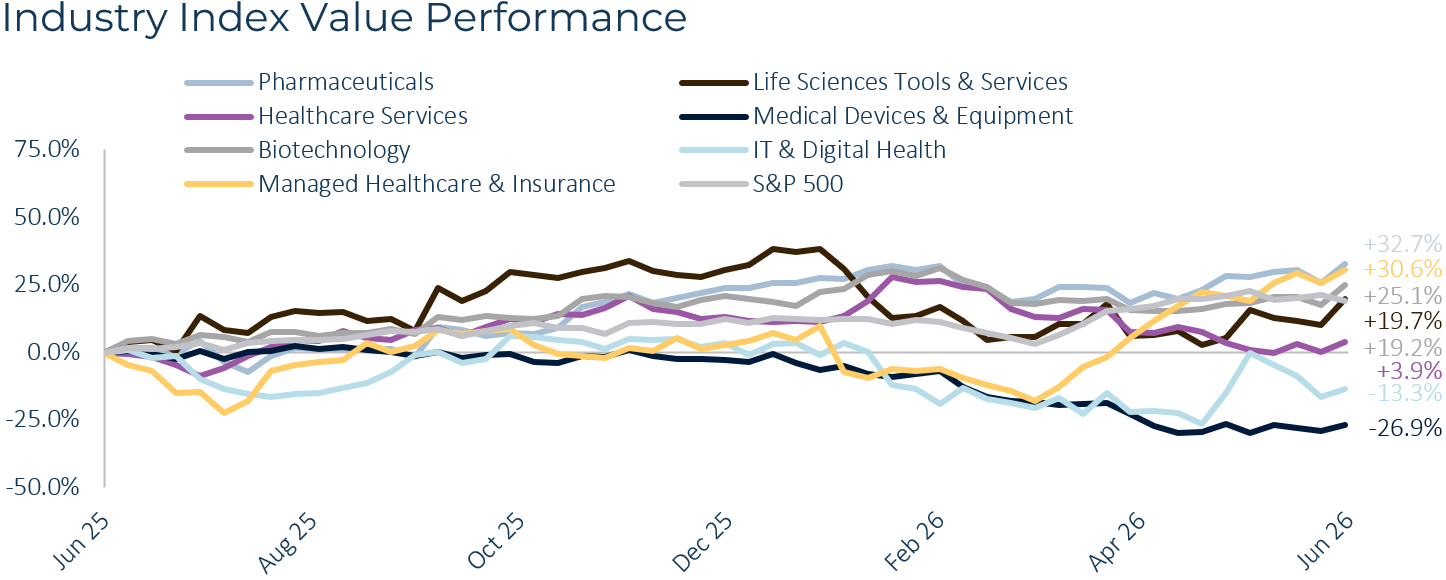

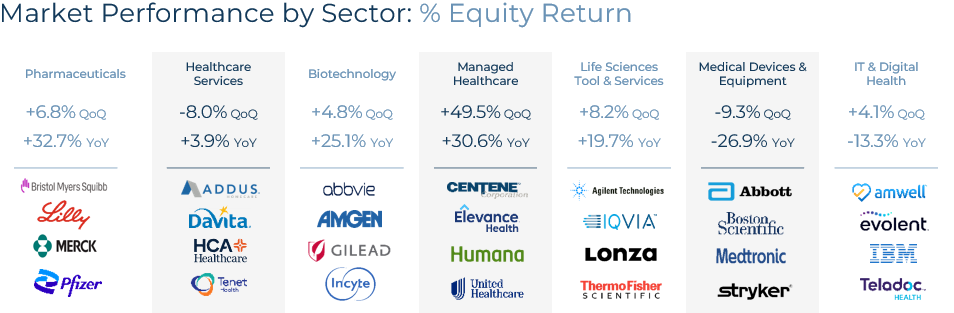

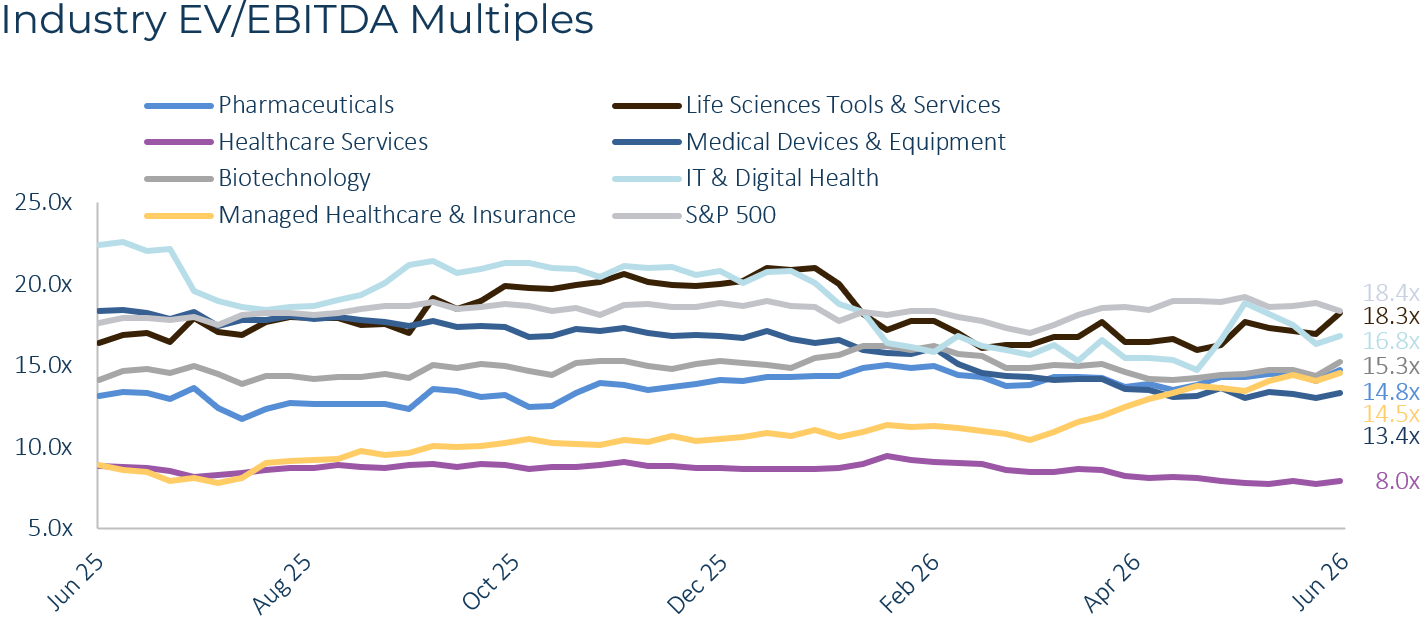

Healthcare delivered a broadly stronger quarter in Q2 2026, though performance varied significantly across subsectors. Most sectors generated positive equity returns as investor sentiment improved alongside a broader market that saw the S&P 500 close the quarter at 18.4x. The gains, however, were concentrated in businesses tied to insurance economics and drug innovation, while medical device manufacturers continued to lag.

Managed Healthcare & Insurance extended its rebound in Q2 after signs of stabilization emerged late in the first quarter. Equity prices surged 49.5% during the quarter as investors gained confidence that the elevated medical cost trends weighing on insurers through 2025 were beginning to normalize. Improving medical cost ratios and the finalized Medicare Advantage rate increase for 2027 helped drive the rebound, with the largest carriers recovering substantial ground as analysts cheered softer cost trends.1,2 Pharmaceuticals also performed well, gaining 6.8% during the quarter and 32.7% over the past year, the strongest trailing-year return in the industry. Biotechnology advanced 4.8%, while Life Sciences Tools & Services rose 8.2%, reflecting continued investor confidence in differentiated science.

The picture was more challenging elsewhere. Medical Devices & Equipment fell 9.3% during the quarter and 26.9% over the past year, making it the industry's weakest performer. The sector continues to absorb margin pressure from tariffs, with roughly 70% of U.S.-marketed devices manufactured abroad and hospital contracts limiting companies' ability to pass higher costs through to customers.³ Healthcare Services also declined 8.0%, while IT & Digital Health stabilized with a modest 4.1% quarterly gain.

These performance trends were reflected in valuation multiples. Managed Healthcare & Insurance experienced the industry's sharpest re-rating, with its EV/EBITDA multiple expanding 4.09 turns to 14.54x. Pharmaceuticals also saw multiple expansion to 14.8x, while Life Sciences Tools & Services maintained the industry's highest multiple at 18.3x. By contrast, Medical Devices & Equipment compressed five full turns year over year to 13.4x, and Healthcare Services now trades at the industry's lowest multiple at 8.0x.

Dinan Index Perspective

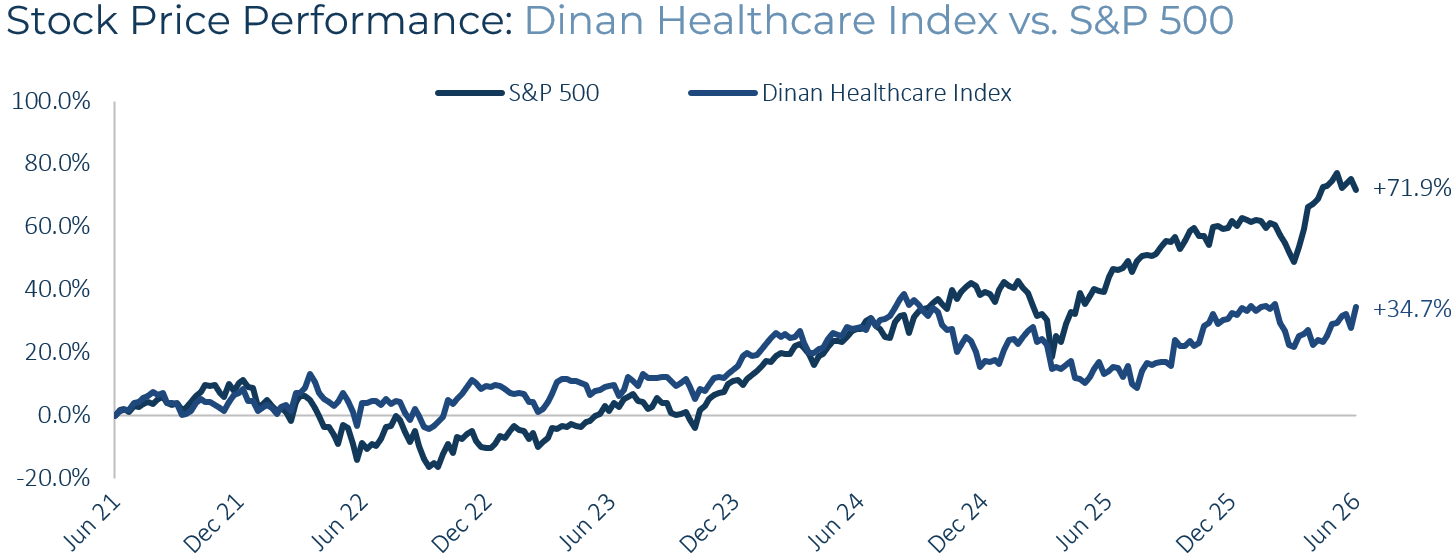

As a supplemental lens beyond broad market indices, the Dinan Healthcare Index† is designed to reflect the public market trends most relevant to middle-market healthcare M&A.

The index reinforced the broader recovery during the quarter, advancing 12.7 percentage points and bringing its cumulative return since inception in 2021 to 34.7%. Recent performance suggests improving sentiment among healthcare investors and is directionally consistent with the recovery observed across public healthcare markets.

Valuations also strengthened. The Dinan Healthcare Index ended the quarter at 14.4x EV/EBITDA, expanding by approximately one turn both quarter over quarter and year over year. While the Index continues to trade below the S&P 500's 18.3x EV/EBITDA multiple, this discount is broadly consistent with the technology-driven nature of broader market returns in recent years. The continued expansion of the Index remains directionally consistent with the broader recovery observed across public healthcare markets.

M&A Activity & Transaction Environment

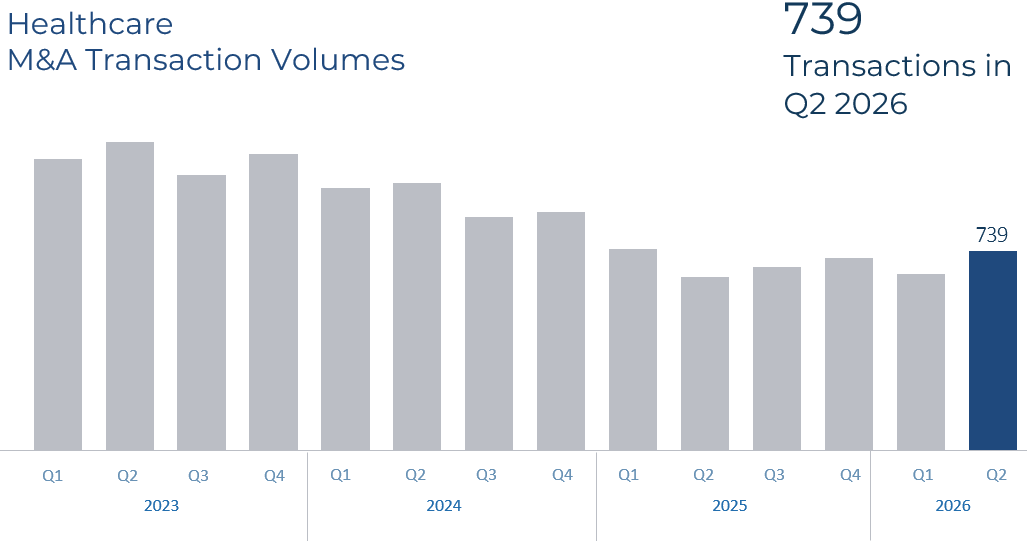

Transaction activity confirmed the renewed optimism. Healthcare deal volume reached 739 transactions in Q2 2026, up 12.8% from the prior quarter and 14.8% from a year earlier, the strongest quarter in more than a year and a clear reversal of the multi-year decline that bottomed in mid-2025.

Biotechnology dominated the deal sheet, consistent with an industry-wide push to replenish pipelines ahead of looming patent cliffs and to deploy capital while valuations recover.4 Larger transactions included AbbVie's roughly $10.9 billion agreement for Apogee Therapeutics and GSK's $10.6 billion move for Nuvalent, alongside Danaher's $10.1 billion acquisition of Masimo in medical devices. Industry-wide, biopharma dealmaking reached approximately $106 billion in the first half, its strongest pace since before the pandemic.5

Financial buyers were equally visible. The quarter included the completed take-private of Hologic by Blackstone and TPG, valued at up to $18.3 billion, a deal that underscored how compressed device valuations are creating openings for private equity to acquire scaled platforms.3,6 The combination of strategic and sponsor demand points to broad-based momentum entering the second half.

Outlook & What to Watch

The durability of the managed care recovery will hinge on whether medical cost trends continue to normalize through the back half of the year. In medical devices, the path of tariff policy remains the key variable for both margins and valuations, even as depressed prices keep the sector in play for acquirers. With biopharma deal momentum running at its fastest pace in years and private equity holding ample capital, the conditions for sustained healthcare dealmaking appear firmly in place.

† The DCA Healthcare Index is Dinan Capital Advisors' proprietary benchmark of carefully selected publicly traded healthcare companies, curated to reflect the public market trends most relevant to middle-market M&A. Index composition is available upon request.

References

1 Modern Healthcare. "UnitedHealth, CVS, Humana forecast 2026 rebound amid higher costs." www.modernhealthcare.com

2 24/7 Wall St. "Humana Jumps 6%, UnitedHealth Climbs 5%, Cigna Rises 4% as Analysts Cheer Softer Medical Cost Trends." 247wallst.com

3 PwC. "Medtech: US Deals 2026 midyear outlook." www.pwc.com; Morgan Lewis. "What Medtech Companies Can Expect in 2026: Regulation, Risk, and Resilience." www.morganlewis.com

4 PwC. "Pharmaceutical and life sciences: US Deals 2026 midyear outlook." www.pwc.com

5 CNBC. "Biotech M&A hits $106 billion, on track for best year since pre-Covid." www.cnbc.com

6 MedTech Dive. "Hologic to go private for up to $18.3B." www.medtechdive.com