The Technology industry regained its footing in Q2 2026, as equity values and valuations improved across most software sectors. Beneath the surface, however, the quarter highlighted a growing divide between the companies enabling the artificial intelligence buildout and the broader software ecosystem still recovering from last year's correction.

Encouragingly, signs of participation began to broaden. While Security and Infrastructure continued to dominate returns, improving performance across several application software categories suggests that the industry's recovery may finally be extending beyond its AI leaders.

The central question heading into the second half of the year is whether software remains a story of AI winners and everyone else, or whether the rest of the market can begin to close the gap.

Sector Performance

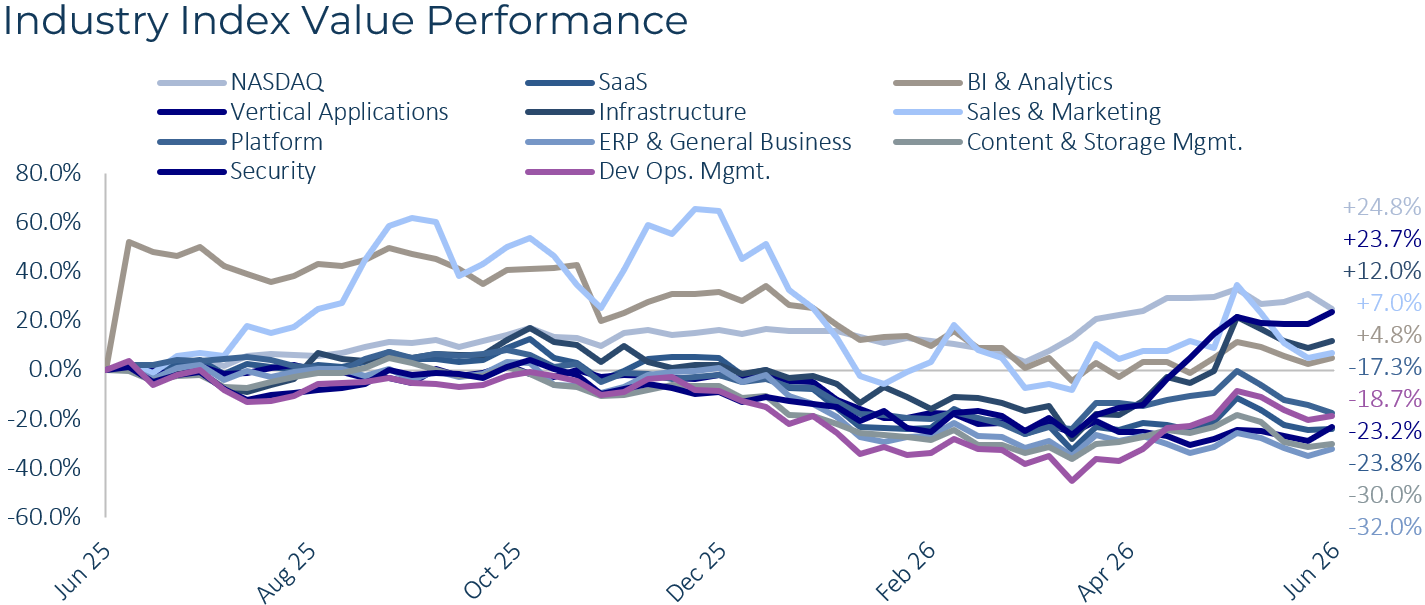

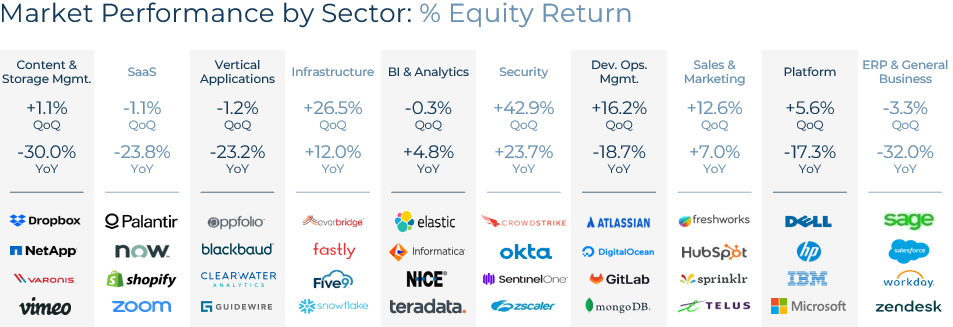

Technology staged a broad recovery in Q2 2026, with positive equity returns across nearly every software sector. The technology-heavy NASDAQ finished up 24.8% over the trailing year, masking a growing divide between the artificial intelligence beneficiaries and the broader application software complex.

The Security sector was the clear standout. Equity prices rose 42.9% for the quarter and 23.7% over the year as investors increasingly viewed cybersecurity vendors as key beneficiaries of enterprise AI adoption.1 Infrastructure delivered the second-strongest performance, with equity values rising 26.5% during the quarter and 12.0% over the year, as the largest hyperscalers are on track to spend more than $600 billion on capacity in 2026, roughly 36% above the prior year.2

Momentum extended beyond the two leaders. Dev Ops Management rose 16.2% for the quarter and Sales & Marketing gained 12.6%, while BI & Analytics maintained a modest 4.8% advance over the trailing year.

The application software complex remained the laggard. ERP & General Business, Content & Storage Management, SaaS, and Vertical Applications all sat roughly 23% to 32% below year-ago levels. However, each stabilized or improved quarter over quarter, providing an early sign that investor sentiment may be beginning to recover.

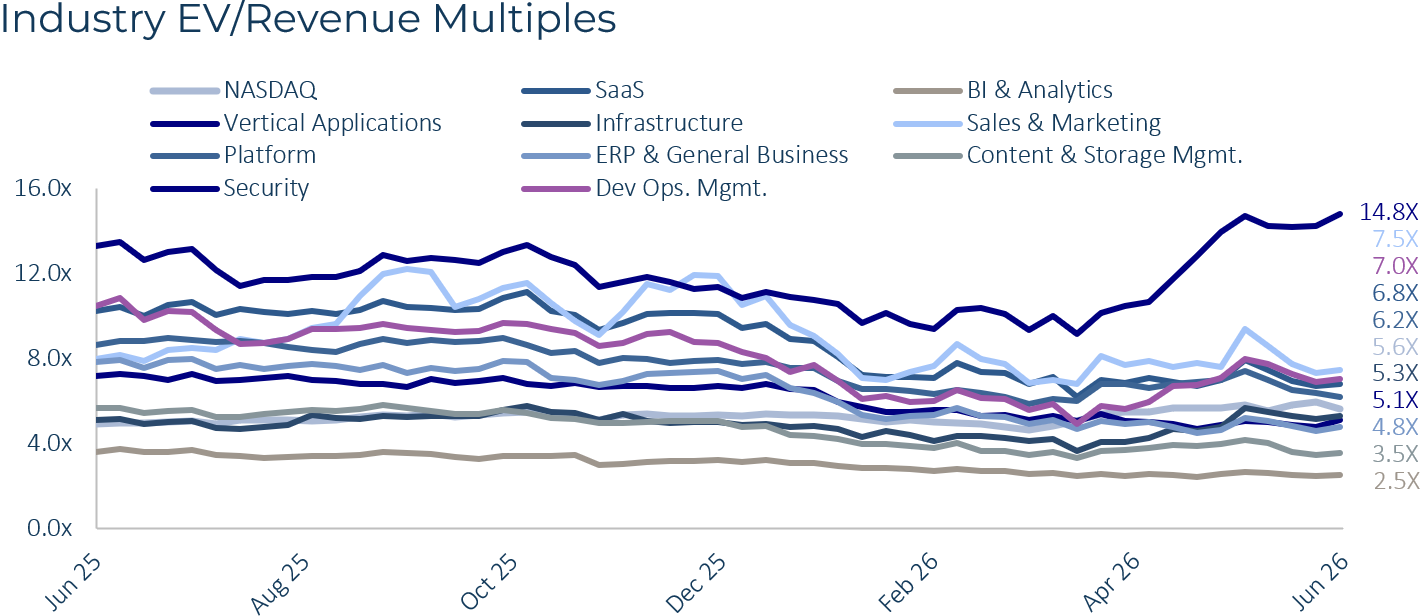

These performance trends were reflected in valuation multiples. Security experienced the industry's strongest re-rating, with its EV/Revenue multiple climbing 58.7% to 14.8x, by far the richest valuation in the sector, while Infrastructure expanded 28.7% to 5.3x. By contrast, the application software complex continued to trade at more modest valuations following last year's compression, although improving multiples suggest the worst of the de-rating may be behind it.

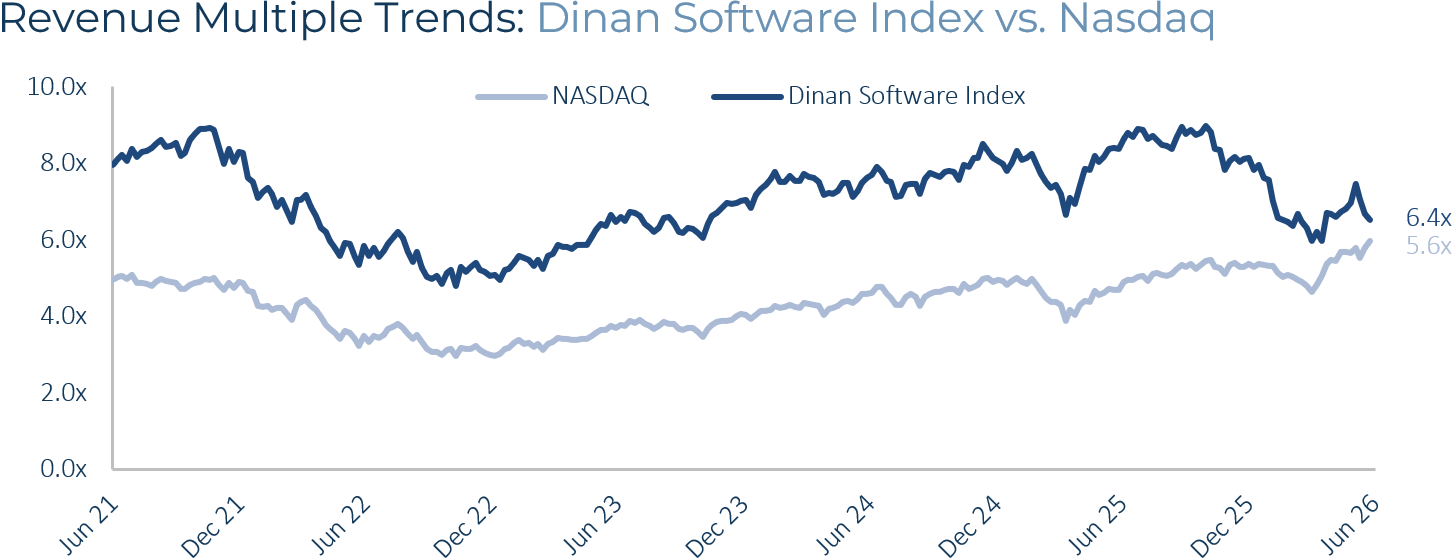

Dinan Index Perspective

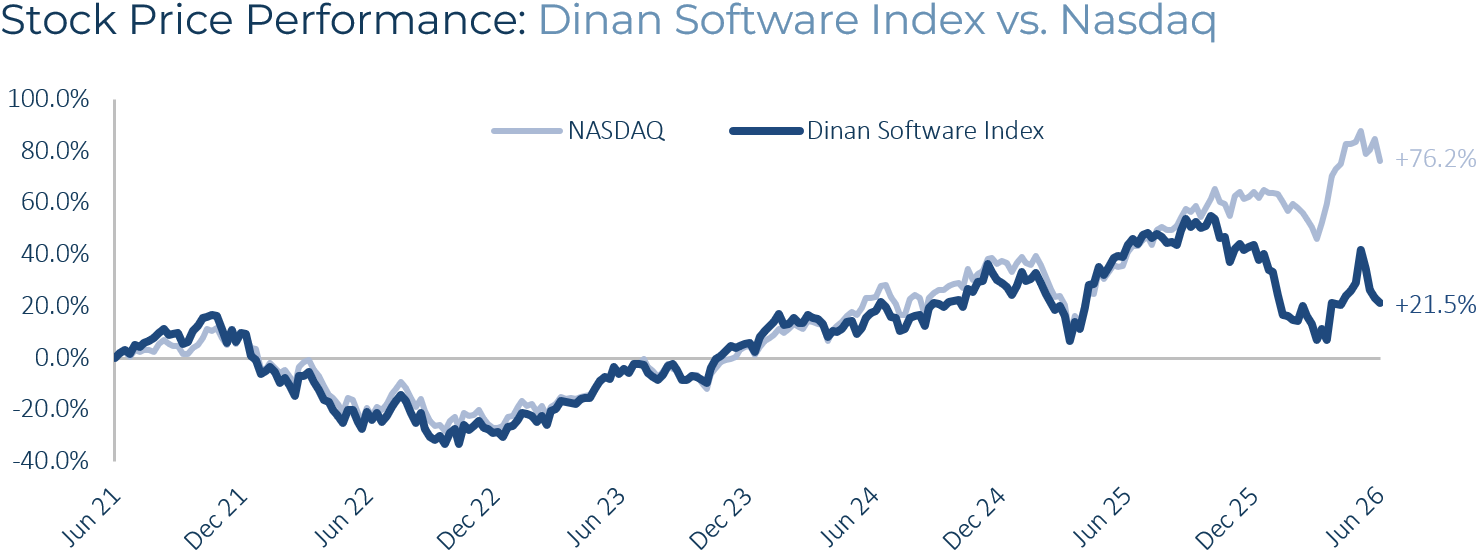

As a supplemental lens beyond broad market indices, the Dinan Software Index† is designed to reflect the public market trends Dinan believes are most relevant to middle-market software M&A.

The index reinforced the growing divergence within technology markets during the quarter. While it has returned 21.5% since its inception in 2021, it continues to trail the NASDAQ's 76.2% return over the same period and declined 15.4% over the trailing year even as the broader benchmark advanced. The gap reflects a public technology market increasingly driven by mega-cap artificial intelligence beneficiaries, while the broader software ecosystem remains earlier in its recovery.

Valuations also reflected this bifurcation. The Dinan Software Index ended the quarter at 6.4x EV/Revenue, above the NASDAQ's 5.6x multiple. Although the index expanded 7.7% during the quarter, it remains 25.4% below its level a year earlier, suggesting that much of the prior multiple compression in traditional software categories has yet to fully reverse. The recent improvement, however, is directionally consistent with broader signs that investor sentiment toward the application software complex may be beginning to stabilize.

M&A Activity & Transaction Environment

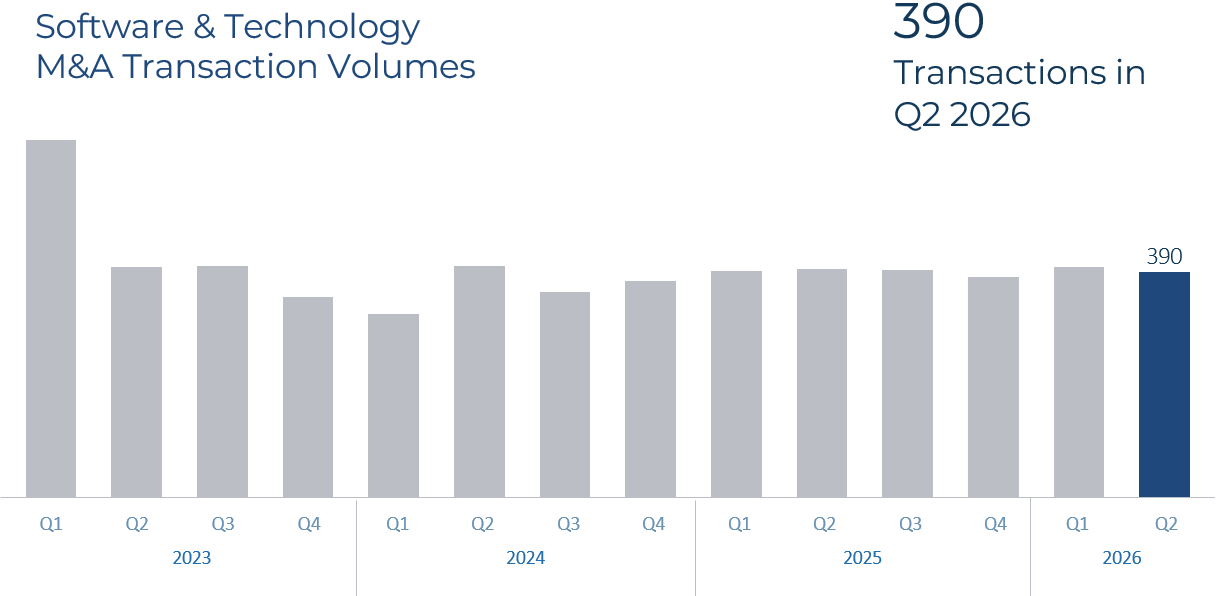

Technology transaction volume totaled 390 deals in Q2 2026, down modestly from 399 in the prior quarter and 395 a year earlier. Volume has held near that level for more than a year, but the steadiness understates the scale of activity, as the quarter produced several of the largest software transactions on record. Sponsors have grown more selective, concentrating capital in higher-conviction targets with clear AI relevance.3

The defining transaction was SpaceX's $60 billion all-stock agreement to acquire Anysphere, the maker of the AI coding tool Cursor, announced June 16 and the largest acquisition of a venture-backed startup on record.4 Private equity was equally assertive on quality assets, as Clearwater Analytics completed its $8.4 billion take-private by a Permira and Warburg Pincus led group on June 25 at a 47% premium, a reminder that sponsors will pay up for durable software.5

Strategic acquirers stayed active as well. ServiceNow's $7.75 billion purchase of cyber exposure specialist Armis underscored the premium buyers place on security, while Qualtrics, Adobe, and Hg pursued targets across the application software space.6 The pattern reflects a market favoring targeted AI acquisitions.

Outlook & What to Watch

The trajectory of AI infrastructure spending remains the most important variable, as it underpins the valuations of the Security and Infrastructure sectors that led the quarter. The central question for the second half of 2026 is whether the lagging application software sectors can convert their quarter-over-quarter stabilization into a sustained recovery. With private equity holding ample capital and having clear appetite for high-quality software at current multiples, the conditions for a broader pickup in middle-market activity are in place.

† The Dinan Software Index is a proprietary index of publicly traded mid-market software companies maintained by Dinan Capital Advisors. Index composition is available upon request.

References

1 Finro Financial Consulting. "Cybersecurity Valuation Multiples Q2 2026." www.finrofca.com; SaaS Mag. "Cybersecurity SaaS Premium: Highest Multiples in 2026." www.saasmag.com

2 CreditSights. "Technology: Hyperscaler Capex 2026 Estimates." know.creditsights.com; IEEE ComSoc Technology Blog. "Hyperscaler capex > $600 bn in 2026, a 36% increase over 2025." techblog.comsoc.org

3 PwC. "Technology: US Deals 2026 Outlook." www.pwc.com

4 CNBC. "SpaceX to acquire the AI coding startup Cursor for $60 billion www.cnbc.com

5 Permira. "Clearwater Analytics Completes $8.4 Billion Take-Private Acquisition by Permira and Warburg Pincus." www.permira.com

6 TechCrunch. "ServiceNow to acquire cybersecurity startup Armis for $7.75B." techcrunch.com